Live Forex News, Live Gold News, Live Indices News & Live Crypto News Today – 10 April 2026

April 10, 2026

Signals Forecast for FX, Gold, Indices and Crypto for Week Starting 13th – 18th April 2026

April 13, 2026

Forex, Gold, Indices & Crypto Outlook for the Week Starting 13 April 2026

The week ahead looks set to be driven by inflation spillover, dollar direction, real yields, earnings season,

and whether geopolitical stress continues to fade. For traders, this is a classic cross-asset environment:

macro data can move currencies, bullion, stock indices and digital assets in the same session.

Executive Summary

The coming week is not simply about one isolated data print. It is about how traders price the full chain:

inflation pressure, central-bank patience, earnings durability, energy-market sensitivity, and the extent to

which recent geopolitical de-escalation can keep risk appetite stable.

In practical trading terms, that means the U.S. dollar remains the central hinge. If markets conclude that

price pressure is still too firm and yields stay elevated, the greenback could reassert control against

lower-yielding currencies and cap upside in risk assets. If inflation fear cools and earnings land well,

cyclicals, growth indices, and high-beta crypto can extend higher while the dollar softens.

Gold enters the week at a technically important point. It is still supported by strategic demand, macro

uncertainty and reserve diversification themes, but short-term price action depends on whether real yields

settle lower. Indices traders should focus on earnings quality, margin commentary and the market’s tolerance

for expensive technology leadership. Crypto traders should watch the same macro drivers as equities:

liquidity, volatility compression, and whether risk-on conditions remain intact.

Key Economic Calendar for 13–18 April 2026

PPI has the power to either reinforce or soften inflation concerns after the latest U.S. CPI data. A firm read

would likely keep markets cautious on rate-cut timing, which is generally supportive for the dollar and can

pressure non-yielding assets in the short term.

Traders will watch for anecdotal evidence on pricing power, consumer demand, labour conditions, margins and

whether energy costs are beginning to flow through into broader business activity. This matters for the dollar,

indices and sentiment-sensitive crypto.

This release matters for EUR crosses because it helps refine expectations around the ECB path. If inflation

confirms firm enough, the euro can stabilize; if the detail looks soft, EUR/USD may struggle to build upside

against a still-resilient dollar.

China data remains important for global risk appetite, commodity-linked currencies, metals and equity sentiment.

A resilient growth pulse would support broader cyclical optimism, while a softer release could lean defensive

across Asia-linked assets and industrial demand proxies.

The March U.S. retail-sales release has been pushed back to 21 April 2026. That means traders should avoid

building this week’s playbook around a data print that is no longer scheduled inside the 13–18 April window.

Forex Forecast

U.S. Dollar Outlook

The dollar remains the market’s macro anchor. After strong headline inflation pressure, the key question is

whether follow-through producer prices and broader business conditions keep Treasury yields elevated. If yes,

the market is likely to reward the dollar again, especially against currencies where central banks remain

closer to easing than tightening.

However, the dollar’s upside is not automatic. If the market decides that the worst of the geopolitical

energy shock is fading and that earnings can absorb some of the cost pressure, the greenback may lose part

of its defensive premium. In that environment, pro-cyclical pairs and carry trades can recover.

EUR/USD

EUR/USD begins the week caught between two forces: euro-area inflation detail and the broader dominance of

U.S. rates. The pair may recover if the full euro-area inflation figures reinforce the case that the ECB

cannot turn too dovish too quickly. But if the dollar remains bid on inflation persistence, rallies may

still struggle into resistance.

GBP/USD

Sterling is likely to trade more as a global risk-and-rate instrument than a pure domestic story this week.

If yields stay firm and the dollar regains traction, cable can remain heavy. A softer dollar and stable risk

backdrop would open the door to recovery, but conviction may remain limited until more fresh UK macro data

lands later in the month.

USD/JPY

USD/JPY remains highly sensitive to the U.S. yield complex. Any renewed rise in Treasury yields would keep

upside pressure alive. If yields pause and volatility softens, the pair could retrace, but sustained dollar

weakness would probably require a broader fall in U.S. rate expectations.

AUD/USD and NZD/USD

Commodity-linked currencies may take cues from China expectations, broad risk appetite and the direction of

the U.S. dollar. If China-related sentiment improves and equity markets remain constructive, AUD and NZD

could outperform. A defensive macro tone would likely reverse those gains quickly.

USD/CAD

The Canadian dollar may remain tied to oil dynamics and general dollar behaviour. If crude stabilizes and

risk appetite improves, USD/CAD can soften. If inflation anxiety brings a fresh bid into the U.S. dollar,

the pair can stay supported.

Weekly Forex Bias

- Neutral-to-bullish USD while inflation and yields remain sticky.

- Mixed EUR until euro-area inflation detail clarifies ECB pricing.

- Selective strength in AUD/NZD only if China and risk sentiment improve.

- JPY vulnerable if U.S. yields rise again.

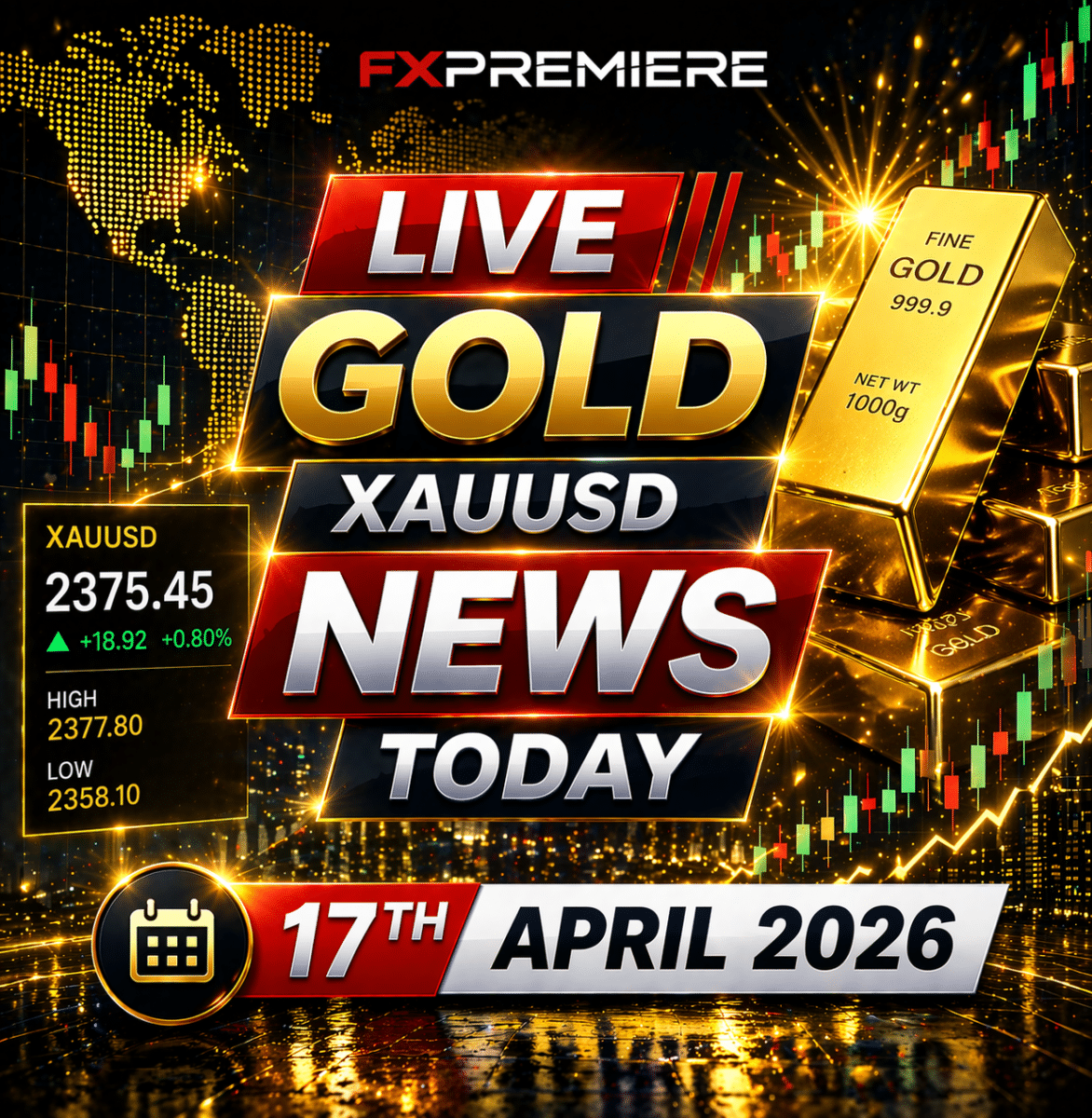

Gold / XAUUSD Forecast

Gold enters the week with two conflicting engines. On one side, bullion still benefits from structural demand:

reserve diversification, geopolitical caution, inflation hedging and long-term distrust of fiat purchasing

power. On the other side, short-term traders remain highly sensitive to real yields and the U.S. dollar.

For XAU/USD, the strongest bullish pathway this week would be a softer dollar, stable-to-lower yields and a

market narrative that inflation pressure is manageable rather than accelerating. That would allow gold to

rebuild momentum and attract both macro funds and momentum traders.

The main bearish risk is straightforward: if producer prices confirm sticky pipeline inflation and yields move

higher again, gold may face another round of profit-taking even if the longer-term macro case stays bullish.

In other words, the strategic story remains constructive, but tactical pullbacks remain possible whenever rate

expectations harden.

What Gold Traders Should Watch

- U.S. dollar direction after PPI and Beige Book tone.

- Real-yield behaviour and whether rate-cut hopes are pushed further out.

- Any deterioration or improvement in geopolitical stability.

- Risk sentiment in equities and whether capital rotates into or out of havens.

Weekly Gold Bias

Constructive but volatile. Gold can remain bid on medium-term dips, but the

cleanest upside extension likely needs yields to stop rising. As long as macro traders view inflation as

sticky but not disorderly, XAU/USD can stay supported overall.

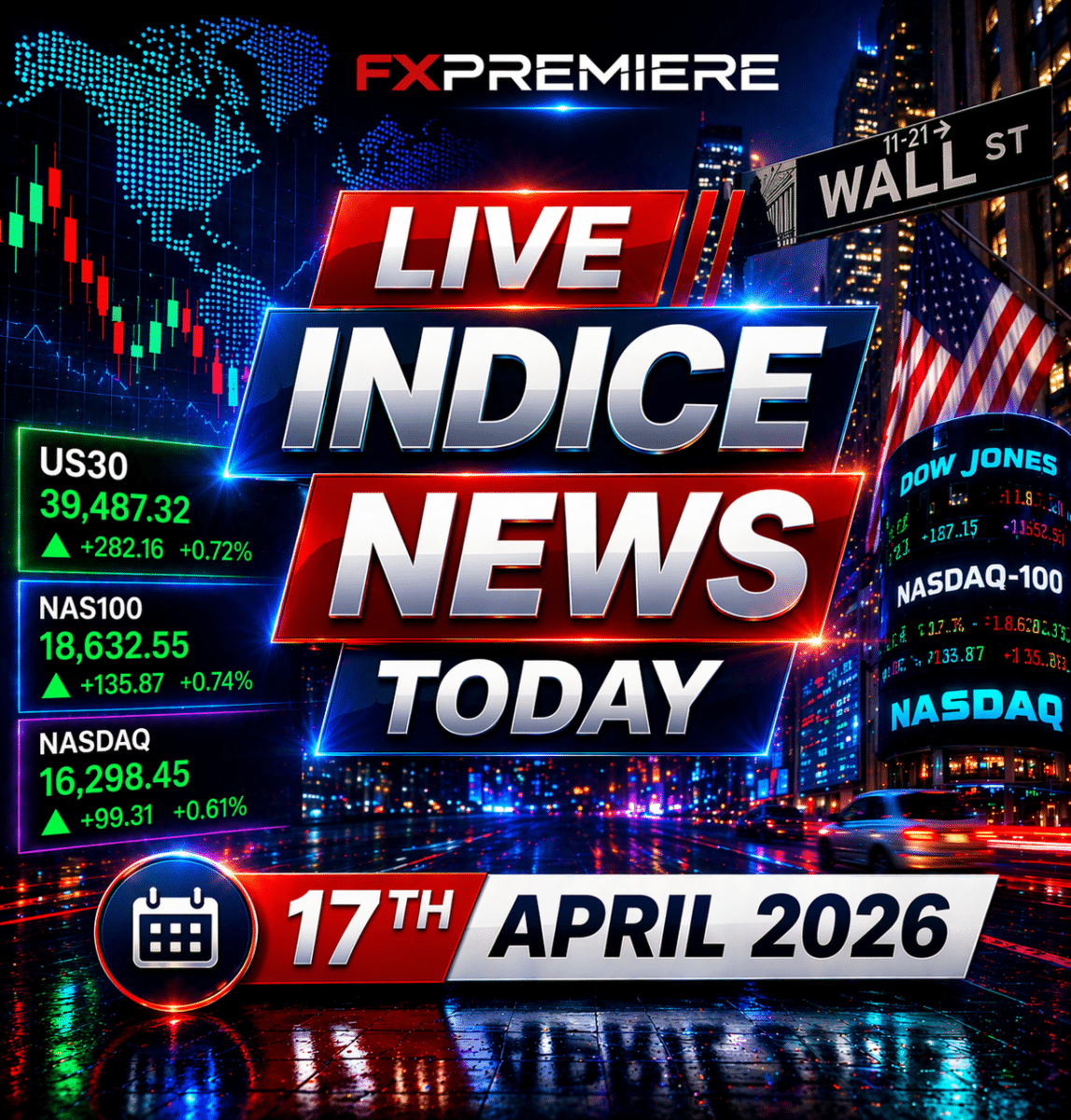

Indices Forecast

Nasdaq / NAS100 Outlook

The Nasdaq remains the most sensitive major index to the balance between yields and earnings confidence. If

earnings commentary from major companies suggests that demand remains healthy and margins can withstand cost

pressure, the growth trade can continue to attract buyers. A calmer geopolitical backdrop also helps.

But if yields resume their climb, richly valued growth names may face renewed valuation compression. That

leaves the Nasdaq in a familiar position: strong long-term narrative support, but vulnerable to any jump in

the discount rate.

US30 / Dow Jones Outlook

The Dow may trade more defensively than the Nasdaq, especially if the market rewards companies with pricing

power, cash flow resilience and less duration sensitivity. Financials and industrials will be important.

Credit commentary from major banks could shape the broader tone of the week.

S&P 500 Tone

The broader U.S. equity tone depends on whether earnings can validate the recent rebound. Markets can absorb

uncomfortable inflation data if revenue growth, guidance and credit conditions remain stable. If executives

begin sounding more cautious on consumers, costs or capital spending, index gains could lose momentum.

What Index Traders Should Watch

- Whether Treasury yields continue rising or flatten out.

- Bank and large-cap earnings guidance.

- Oil-price sensitivity and the effect on inflation expectations.

- Whether cyclical leadership broadens beyond a narrow group of mega-caps.

Weekly Indices Bias

Cautiously bullish while earnings remain supportive and geopolitical stress

continues to ease. The biggest threat to upside is a renewed inflation-rate shock that pushes yields sharply

higher.

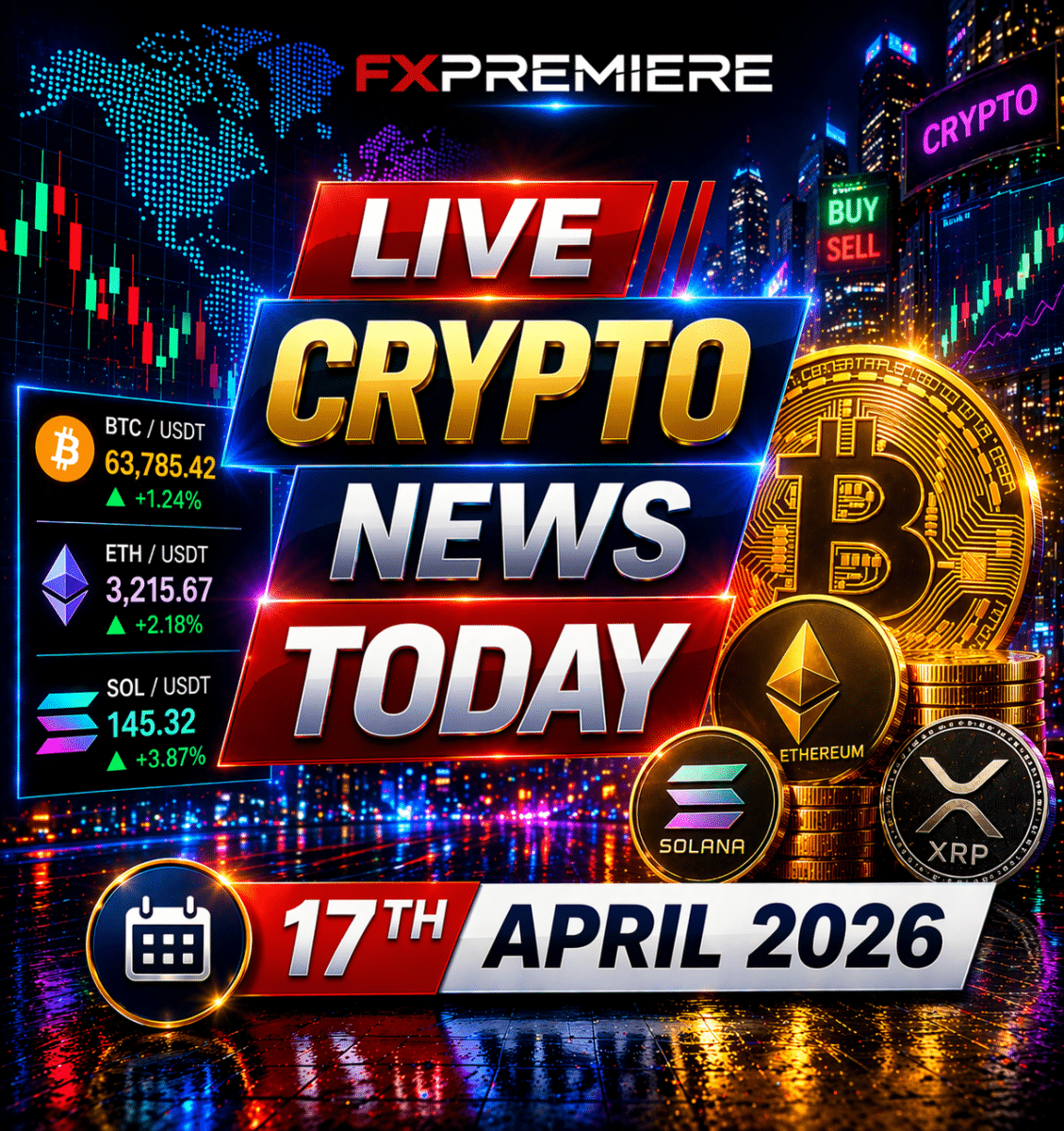

Crypto Forecast

Crypto heads into the new week with improving sentiment, but the market is still trading as a macro-sensitive

risk asset rather than a disconnected universe. Bitcoin and Ethereum can continue to benefit from calmer

headlines, improving appetite for speculative risk and a stable liquidity backdrop. However, upside remains

vulnerable if real yields jump or the dollar strengthens aggressively.

For Bitcoin, the bullish case is that macro fear continues to cool, equities stay firm, and capital rotates

back into high-beta assets. For Ethereum, relative performance may depend on whether traders embrace the

broader digital-asset complex rather than hiding only in Bitcoin strength.

Crypto traders should remember that this is still the same macro week: PPI, Beige Book, yields and the dollar

all matter. A friendlier macro tape can support continuation higher. A hawkish repricing across rates markets

can quickly cool momentum.

Weekly Crypto Bias

- BTC: Bullish while risk appetite remains constructive.

- ETH: Bullish but more sensitive to overall market breadth.

- Altcoins: Selective; strongest if BTC holds trend and volatility stays orderly.

- Main risk: A stronger USD and higher yields can trigger fast de-risking.

Market Bias & Trading Scenarios for the Week

Scenario 1

Sticky inflation + higher yields

USD firmer, gold choppy, Nasdaq vulnerable, crypto upside capped.

Scenario 2

Inflation fear cools + earnings hold up

Risk assets extend, dollar eases, gold recovers, BTC/ETH stay supported.

Scenario 3

China data beats

AUD, NZD, commodities, Asian risk and cyclical equities gain relative support.

Scenario 4

Geopolitical stress returns

Safe-haven demand reappears, oil volatility rises, indices and high-beta assets turn defensive.

FXPremiere Weekly Trading View

Base case for the week of 13–18 April 2026: mixed-to-volatile markets with the U.S. dollar still at

the center, gold structurally supported but yield-sensitive, indices dependent on earnings quality, and

crypto supported as long as macro stress does not re-accelerate.

This is a week to stay flexible, respect macro headlines, and avoid overcommitting to one narrative too early.

The cleanest setups are likely to appear after the market digests inflation-linked signals and earnings tone.

The only official free FXPremiere Telegram channel is

https://t.me/forexsignalstrialgroup

and the only official live chat/support is

https://t.me/forexsignalssms.

All other Telegram channels claiming to represent FXPremiere are fake or scam channels. Always verify through

FXPremiere.com.

Frequently Asked Questions

What is the most important driver this week?

The most important driver is the interaction between inflation expectations, Treasury yields and risk sentiment. That combination will shape the dollar, gold, indices and crypto together.

Is gold still bullish this week?

Gold remains constructive on a medium-term basis, but short-term price action can still swing sharply if U.S. yields rise again. Tactical volatility does not necessarily invalidate the larger trend.

Which asset class is most sensitive to yields right now?

Nasdaq-linked indices and parts of the crypto market remain especially sensitive to rate expectations and real yields, while gold also reacts quickly to changes in the dollar-yield mix.

Why does China matter for this forecast?

China matters because it influences commodity demand, global cyclical confidence, Asia-linked currencies and overall risk appetite. Stronger Chinese growth can help broader sentiment; weaker prints can do the opposite.

🔗 For reliable GOLD signals, visit GoldSignals.co.

Latest Market Updates

Are There Any Recommended Telegram Channels for Crypto Trading Signals?What Factors Should I Consider When Choosing a Forex Signal Provider?What Factors Should I Consider When Choosing a Forex Signal Provider?

How Can I Find Reliable Signals for US30 and NAS100 Trading?

What Are the Best Strategies for Trading XAUUSD Effectively?

Crypto Signals News Forecast Starting 17th April 2026

Indice Signals News Forecast Starting 17th April 2026

Gold XAUUSD Signals News Forecast Starting 17th April 2026

Forex Signals News Forecast Starting 17th April 2026

Discipline in Trading: The Real Secret to Success

How to Build a Consistent Trading Plan

Latest Trading Signals & Market Insights

Explore forex signals, gold signals (XAUUSD), crypto signals, and indices signals from FXPremiere.com — a global leader in trading signals.

{kind=link}

{kind=link}

{kind=link}